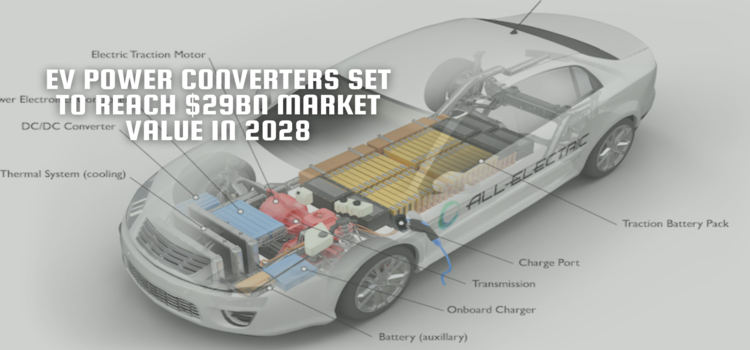

Yole Developpement predicts that the market value of power converters for xEV vehicles will reach $29 billion by 2028, with a 12.2% CAGR between 2022 and 2028, thanks to continuous cost reduction. With the entry of new consumer electronics players such as Xiaomi and Sony, existing Tier 1 suppliers could find new opportunities.

The global light duty vehicle market is swiftly transitioning towards electrification, with xEVs estimated to hold a 53.5% market share out of 93 million units in 2028. Among various electrification technologies, BEVs lead the market with a 19.1% CAGR between 2022 and 2028, while the annual growth of xEV in general over the same period is 14.1%. The ICE market is collapsing in some countries leading the way in electrification. For instance, in China, NEV market share surged from 13.4% in 2021 to 25.6% in 2022.

Tesla aims to achieve cost parity with ICE, reducing costly SiC usage through technological innovations, sourcing practices, and fleet strategies. BYD has also recently launched C-class PHEV models at prices similar to ICEs from peer brands. Electrification extends beyond passenger vehicles, with increasing adoption of electric light commercial vehicles for last-mile delivery requiring specific models with synergies with passenger or medium-duty commercial vehicles.

China leads in vehicle electrification with a local supply chain mixed with international players. Local Tier 1 suppliers are emerging, while Tier 2 suppliers continue to be dominated by international businesses. Automotive power devices now have an interest in both Si IGBT and SiC MOSFET. Chinese OEMs are focused on in-house power module packaging, which demonstrates their strong focus on automotive semiconductor since before the COVID pandemic.

日本語

USD $